As an owner of a small business or a freelancer, a Simplified Employee Pension (SEP) is considered a more beneficial retirement plan than a standard IRA. With higher contributions and simplified processes, SEP IRAs offer flexibility and low administration costs.

Throughout this in-depth guide, Gold IRA Blueprint discusses what SEP means, eligibility, contribution limits, and more. You will also find out the answers to questions about how SEP works and what its flaws are.

Key Takeaways

- SEP IRA is a simplified employee pension plan that an employer or a self-employed individual can set up.

- A SEP-IRA plan is much like a traditional IRA with tax-deferred contributions and growth.

- If you make a contribution to yourself, you should proportionally contribute to each of your eligible employees.

- SEP IRA plan contributions are flexible, allowing you to skip a year when the business is not making a profit.

- SEP IRA plans offer high contribution limits of up to $66,000 in 2023.

What Is a SEP IRA?

A SEP IRA stands for Simplified Employee Pension, and it is an individual retirement account that an employer or a self-employed individual can set up. A SEP-IRA plan is suitable for people who work as freelancers, own a business, and employ others. Having a Simplified Employee Pension allows employers to contribute to their own retirement accounts as well as their employees.

This IRA is called simplified for a reason. A SEP-IRA plan is suitable for small businesses or self-employed individuals, and it is straightforward to set up and maintain. Much like a traditional IRA, SEP IRA contributions are tax-deductible, while the growth of your investment is also tax-deferred until retirement.

One of the notable advantages of setting SEP IRA plans is that employers are not required to contribute every year. Moreover, employers can benefit from either increasing or lowering the contributions to their employees based on the profits made that year.

Who Is Eligible for a SEP IRA?

SEP IRA plans are designed for self-employed individuals or those who own small businesses. Ideally, if you run a business, you should have a few employees. If your employees are eligible for a SEP IRA account, you will be required to match their percentage of contribution to your own. This means if you decide to invest 15% in your own SEP-IRA plan, you will have to do the same for your employees.

So, to understand if your employees qualify for SEP IRA, they should:

- Be 21 years of age or older

- Work for your business for at least three years of the past five years

- Receive a compensation of $750 in 2023 or 2024, $650 in 2021 and 2022, or $600 in 2016-2020

You can set up a SEP account with requirements that allow you to enroll in the plan immediately. Later, you can also amend the eligibility requirements for future employees, making them stricter. However, it should be done in a way that you, as an employer, meet those new requirements, too.

The amendments can include the length of work. For example, you can choose to enroll employees who have worked for your company for three years, or you can let them enroll in the retirement plan as soon as they start their employment. The same applies to age restrictions, which means employees who are 18 and older can enroll in the plan.

Who May Be Excluded from the SEP IRA Plan?

You can exclude employees who do not meet the requirements set in your SEP IRA plan: work length, age requirement, and the amount of received compensation.

If your employee is a non-US resident with no US source compensation, you may also exclude them from your SEP plan.

Employees covered by a union agreement may also be excluded if their retirement benefits were bargained for by you and the union.

How Does a Simplified Employee Pension (SEP) Work?

Having a self-employed SEP IRA plan, you decide on how much to contribute towards your retirement and can choose to skip a year if needed. That being said, the contribution shouldn’t be higher than 25% of your net earnings. In 2022, the limit for a self-employed SEP plan was $61,000.

Different rules apply if you own a company and hire employees. As an employer, you are required to make equal contributions to all eligible employees. The downside here is that if a selected employee dies or quits during the year when your plan is active, you must contribute regardless of the circumstances.

To set up a SEP IRA plan as a business owner or a freelancer, you should:

- Create a formal written agreement either through your financial institution or using IRS Form 5305-SEP.

- Provide your eligible employees with all the necessary information. The instructions are usually included in Form 5305-SEP.

- Set up individual SEP IRA plans for each eligible employee that they will own and manage.

Once set up, you can use your SEP IRA to invest in gold, silver, or other tangible assets to shield yourself from inflations.

What Is a SEP Contribution Limit?

If you have employees, your contributions to their SEP IRA plans should not exceed the lesser of 25% of compensation or $66,000 for 2023. The employee contributions must be proportional and be of the same percentage of salary.

As a sole business owner and worker, you can also contribute to your SEP IRA plan. The contribution is limited to 25% of net profit minus one-half of the self-employment tax and minus your SEP contribution.

Each SEP contribution can later be deposited into a traditional IRA. All SEP contributions are 100% vested, and employees can manage their investments from their own separate accounts. However, employees are not allowed to make SEP IRA contributions themselves.

SEP IRA Rules and Restrictions

SEP IRA Income Limitations

The SEP-IRA contributions have certain limitations when it comes to employee income. The employee’s contribution should not be higher than 25% of compensation or $66,000 for 2023, whichever is less.

The amount of compensation is also limited to $330,000 for 2023 ($305,000 for 2022 and $290,000 for 2021).

The contributions to the SEP-IRA plans are 100% vested. However, an employee or a business owner may only borrow the maximum amount of $50,000 or 50% of the account balance, whichever is less. This means if you have $90,000 in your vested account, you may take up to $45,000, or if you have $150,000, you may only take a loan of $50,000.

Withdrawals and Contributions

SEP contributions are tax-deferred and can be taken at any time. It’s important to note that SEP IRA plans do not offer catch-up contributions for employees since SEP accounts are funded only by employers.

The withdrawals are taxable, and if you decide to take some savings before the age of 59 ½, the tax of 10% will be applied.

Minimum Distributions Rules and Rollover

Every SEP IRA plan holder can have their earnings and contributions rolled over to other IRA accounts. The rollover is tax-free and can be transferred to:

- Roth IRA

- Traditional IRA

- SIMPLE IRA (only after 2 years)

- Governmental 457(b)

- Qualified Plan

- 403(b)

When you turn 73, you will have to start taking required minimum distributions (RMDs) in accordance with the IRA rules.

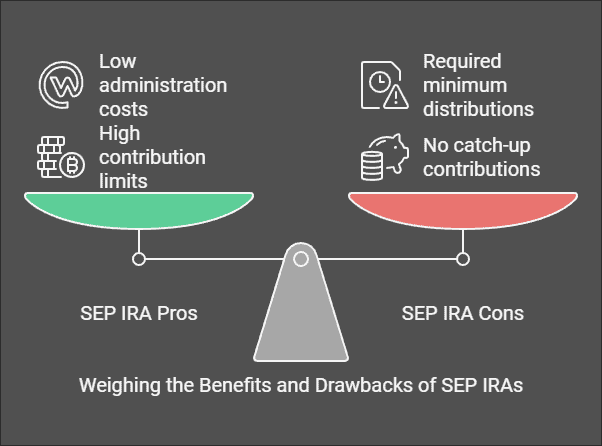

Pros and Cons of SEP IRA

| PROS | CONS |

| + High contribution limit of up to $66,000 in 2023 + Low administration costs + Flexibility to skip a year if a business is down + Contributions are 100$ vested and tax-deferred |

– No catch-up contribution for 50 or older – Equal percentage of contributions to each eligible employee if you contribute to yourself – Required minimum distributions at the age of 73 – 10%-taxed distribution when taken at the age 59 ½ or younger |

Frequently Asked Questions

What Is a SEP IRA Plan?

SEP retirement plans are individual retirement accounts designed for self-employed individuals or owners of small businesses with or without employees. If you open a SEP IRA account, you should also set it up for each of your eligible employees. The eligibility requirements may vary, depending on what limitations you apply to your SEP plan.

How do I invest my SEP IRA?

Your financial institution may offer to invest in stocks, bonds, or mutual funds. There may be other investment options available, but they will depend on your account provider.

Do I have to contribute to the SEP-IRA account of an employee who is over 70?

The contributions to your eligible employees’ SEP IRA plans should be equal, regardless of age. This means you must contribute to the SEP-IRA of your employee who is over 70.

Can I set up a SEP as a self-employed individual while taking part in another retirement plan at another job?

Yes, you can set up a SEP IRA for yourself if you own a self-employed business. This plan will not interfere with or cancel out the retirement plan you are enrolled in at your second job.

What should I do if my employee doesn’t want to participate in the SEP IRA?

Since an employer must make equal contributions to all eligible employees, you will still be required to set up a SEP IRA plan for the employee who is not willing to have one.

What is the maximum contribution amount to the SEP?

The employer’s contributions to employees’ SEP IRAs cannot be higher than 25% of compensation or $66,000 in 2023, whichever is less.

Do I have to contribute to the SEP every year?

The flexibility of SEP retirement accounts might be their biggest advantage. If your business suffers from a loss or the profits are too low, you can miss out on years. However, if you do contribute, then you have to include all eligible employees.

Article Sources

At Gold IRA Blueprint, we dive deep into the world of gold IRAs, using trusted sources to back up our insights. Our sources range from official documents to expert interviews, ensuring our content is both accurate and reliable. We also draw on research from reputable publishers to give you the most comprehensive understanding possible. Check out our editorial policy to see how we maintain our high standards for accuracy and fairness. Also make sure to check out our Financial Review Process to have a better understanding of our process.

https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-seps

https://www.investopedia.com/terms/s/sep.asp#citation-27

https://www.forbes.com/advisor/retirement/sep-ira/

Authors & Disclosures

- Our content is independently written and reviewed by trusted reviewers & fact-checkers.

- We can earn money by connecting you with top Gold IRA Companies. Learn how our reviews work.

- Want to learn more? Meet our authors and explore our editorial policy.